Economic policy has changed dramatically since the Great Recession. The post-WWII liberalising trend in goods trade is being reversed and multilateral cooperation is ceding ground to a more nationalistic view of policy (World Bank 2020). At the same time, technological change is accelerating, especially in response to the COVID-19 shock. In this changing environment, it has been possible to closely track goods trade policies, but there is much less information on how services policies have evolved despite the growing importance of services in output and trade (WTO 2019).

This gap in information matters because services are intimately linked to developments over the last decade. For instance, the Great Recession originated in financial markets where regulation failed to keep step with liberalisation (Rajan 2010); the emergence of new digital platforms is transforming business, retail, communication, transport, and financial services; and the improvements in information and communication technology could be ushering in a new era of cross-border trade in services (Baldwin 2019). Are governments reacting to these developments proactively through radical reform, defensively by imposing new restrictions, or inertially by doing nothing?

To answer this question and to facilitate the empirical analysis of policy change, the World Bank and the WTO engaged in a major policy data collection and quantification exercise, which resulted in a new World Bank-WTO Services Trade Policy Database (STPD).1 This database contains information on the services trade policies in five broad areas – financial, telecommunication, distribution, transportation, and professional services.2 The STPD contains information not just on core trade policies but also on other increasingly relevant regulatory measures such as licensing conditions and restrictions on cross-border data flows.

Policy restrictiveness is quantified following an improved Services Trade Restrictions Index (STRI) that aggregates the qualitative information within a single consistent and transparent measure. Data previously collected by the World Bank over 2008-2011 were adjusted to the new classification and quantified based on the updated STRI methodology. The harmonised data make it possible for the first time to compare services trade policies over a long period of time – between 2008 and 2016 – for a large cross-section of 55 advanced and developing economies.

On the basis of that information, it is possible to identify patterns of services trade policies across economies and sectors as well as secular trends in policy making over the past decade. On the face of it, services trade regimes are generally becoming more open, at least as far as explicit restrictions are concerned, in apparent contrast to recent changes in goods trade policy. Most recently, however, services trade policy is also becoming more restrictive, especially in digitally traded computer and audio-visual services (OECD 2020). Tightening measures in 2019 mostly affected foreign investment and the movement of people.

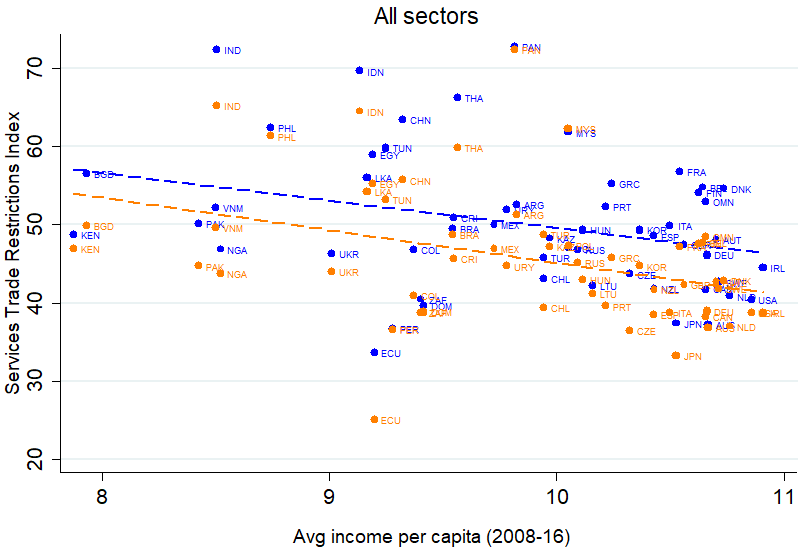

This most recent turn of events notwithstanding, higher income economies are still more open on average than lower income economies in most sectors. The decrease in policy restrictiveness since 2008, i.e. over nearly a decade, is slightly more pronounced for high-income economies (Figure 1). At the same time, some dynamic developing economies such as Bangladesh, India, and China have also liberalised significantly in the past decade. Other lower-income and middle-income economies that have liberalised their services trade policies appreciably (by at least five points on average) are Ecuador, Uruguay, Indonesia, Tunisia, Thailand, Colombia, Costa Rica, and Pakistan. Underlying these patterns of overall liberalisation across economies are differences in the sectoral pattern of liberalisation. We illustrate these below by focusing on two sectors: financial services (especially commercial banking) and professional services (auditing).

Figure 1 Services trade policy has become more open since the Great Recession (Changes in STRI between 2008-2011 and 2016 by level of income)

Note: STRI 2008-11 in blue, STRI 2016 in orange.

All sectors have been liberalized but by varying degrees. Broad waves in services policy reform can be identified. Higher income economies have led the way, pioneering the opening up of telecommunications and finance to foreign competition in the 1980s and 1990s. Hence, the picture already emerging a decade ago in these two sectors was of general openness in higher income economies, and of varying degrees of liberalisation in developing economies. The new database reveals that since 2008 developing economies have started to reform those sectors that were first liberalised by higher income economies, while the latter have embarked on the liberalisation of other sectors, notably professional and transport services. Hence, the picture emerging more recently is of policy convergence in telecommunications and finance driven by liberalisation by hitherto more restrictive developing economies, and divergence and dispersion in sectors such as professional and transport services.

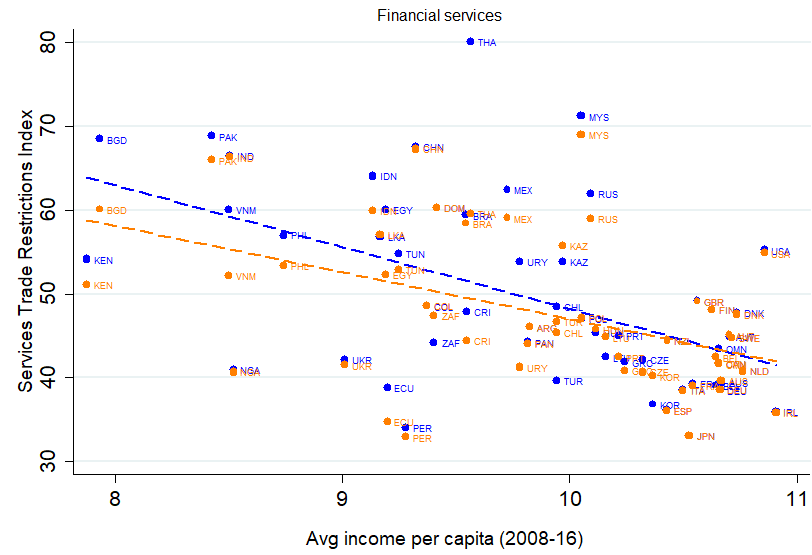

There are particularly striking examples of recent reforms in financial services in some of the most dynamic developing countries such as Bangladesh, Kenya, the Philippines or Vietnam (Figure 2).

Figure 2 Limited convergence in financial services trade openness (Changes in STRI between 2008-2011 and 2016 by level of income)

Note: STRI 2008-11 in blue, STRI 2016 in orange.

Digging deeper into the policy data on commercial banking services reveals certain patterns. A large majority of economies now allow entry into their markets through the acquisition and control of domestic entities, through the establishment of wholly owned subsidiaries, or through direct branching. The preferred avenue is the acquisition of already licensed institutions, which may be explained by the host regulators’ wish to recapitalise local banks (notably after the 2008-2009 financial crisis) while maintaining the existing market structure and therefore the current intensity of competition. Both fully owned subsidiaries and direct branches have been increasingly allowed in most economies, but the former remains a preferred option for local regulators, given the potential for risk transmission that foreign bank branches present, as was evident in the financial crisis. Interestingly, no economy in our sample abrogated access through branching – the increased share of governments allowing this form of entry is the result therefore of additional liberalisation in emerging economies (e.g. Colombia, Egypt, Indonesia, Philippines, Russian Federation).

Even though there are now fewer explicit restrictions on entry, scrutiny of foreign banks has remained intense or even been strengthened. For instance, even when the presence through branching is allowed, stringent regulatory conditions (e.g. imposition of endowment capital requirements, limitations on the expansion of the branching network) are imposed in a majority of economies. In addition, roughly a quarter of our sample now applies different licensing criteria for foreign banks. Finally, more than half of the economies in our sample subject foreign banks to either economic needs tests, investment screening requirements or non-automatic licensing approvals (even when all formal licensing criteria have been fulfilled).

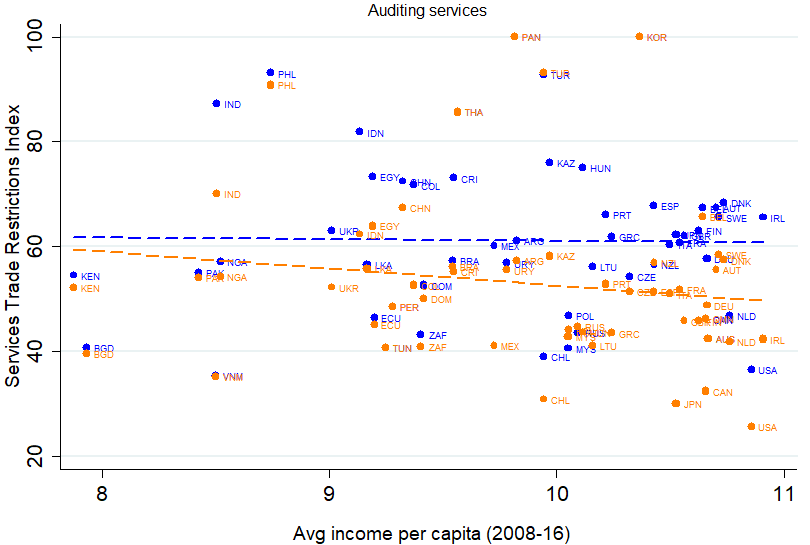

Figure 3 Divergence in auditing services trade openness (Changes in STRI between 2008-2011 and 2016 by level of income)

Note: STRI 2008-11 in blue, STRI 2016 in orange.

Policy dispersion is still the norm in sectors that joined the liberalisation wave more recently and in a more limited number of economies. In auditing, most of the decrease in the STRI is linked to less restrictive policies regarding the entry of professionals in high-income and middle-income economies, as well as the loosening of restrictions for cross-border supply for high-income economies. Restrictions on commercial presence were reduced only slightly, with highly restrictive economies remaining so in 2016 (India, Korea, Panama, the Philippines, Turkey).

The high-income economies presenting the biggest reductions in restrictiveness are Japan and some EU members, where reforms in the auditing subsector came into force in June 2016 in the aftermath of the financial crisis. One of the aims was to improve auditing quality, and to introduce rotation of auditors because of the concentration of the market. One of the tools envisaged in that regard was to facilitate cross-border provision of statutory audit services. Focusing more specifically on the temporary movement of natural persons supplying services, restrictions have decreased since 2008-2011 in European economies and in some other high-income countries (e.g. Canada, Japan, US). This was accomplished either by relaxing some of the economy-wide restrictions on the movement of persons (quantitative limitations), the lifting of nationality or residency requirements to obtain a license to practice, or the recognition of foreign qualifications.

To conclude, the last decade has seen steady and widespread liberalisation, but with a twist. While markets in services, e.g. finance and telecommunications, are increasingly free from explicit restrictions on entry and ownership, they are increasingly subject to greater regulatory scrutiny (e.g. economic needs tests, FDI screening), especially in higher income economies. This raises several questions for future analysis. Does this type of measure reflect ‘learning-by-liberalising’, in that lessons have been learnt on the need to complement openness with more stringent prudential regulation? Do they reflect a shift analogous to the reversal of openness in goods trade policy, ostensibly on security grounds, but possibly in response to the increased competitiveness of developing economies’ services firms? And do they signal a trend towards de jure openness but de facto discretionary policy, in particular at the point-of-entry stage (e.g. through FDI)? These policy trends deserve further analysis.

References

Baldwin, R (2019), The Globotics Upheaval: Globalization, Robotics, and the Future of Work, Oxford: Oxford University Press.

Borchert, I, B Gootiiz and A Mattoo (2014), “Policy Barriers to International Trade in Services: Evidence from a New Database”, World Bank Economic Review 28(1): 162-188.

Borchert, I, B Gootiiz, J Magdeleine, J A Marchetti, A Mattoo, E Rubio and E Shannon (2019), “Applied Services Trade Policy: A Guide to the Services Trade Policy Database and the Services Trade Restrictions Index“, WTO Staff Working Paper ERSD-2019-14 and World Bank Policy Research Working Paper 9264.

Borchert, I, J Magdeleine, J A Marchetti and A Mattoo (2020), “The Evolution of Services Trade Policy Since the Great Recession“, WTO Staff Working Paper ERSD-2020-02 and World Bank Policy Research Working Paper 9265.

OECD (2020), Services Trade Restrictiveness Index: Policy Trends up to 2020, Paris: OECD.

Rajan, R (2010), Fault Lines: How Hidden Fractures Still Threaten the World Economy, Princeton: Princeton University Press.

World Bank (2020), World Development Report: Trading for Development in the Age of Global Value Chains, Washington, D.C.: World Bank.

WTO (2019), World Trade Report: The Future of Services Trade, Geneva: WTO.

Endnotes

1 The first international database of services trade policy created by the World Bank had policy mostly pertaining for the year 2008, just pre-dating the financial crisis

2 The dataset is being expanded to cover computer, construction, health, and tourism related services.

To read the Original blog, click here