The tax reform bills that have now passed both the House and and Senate look to have more tax cuts than base-broadening reforms, at least in the next few years.

The main impact of tax reform on the trade balance thus will come from the rise in the fiscal deficit.

Because the tax cuts are front-loaded, the Senate proposal would increases the fiscal deficit by a bit more than one percent of GDP in the next few years —see the CBO forecast (The projected peak increase in the fiscal deficit comes in fiscal 2020, with a peak impact of $250 billion or around 1.2 percent of GDP). The fiscal impact of the tax cuts then starts to fade out. The U.S. general government fiscal deficit (the IMF’s preferred measure, which includes state and local borrowing) should rise from its current level of around 4 percent of U.S. GDP to around 5 percent of U.S. GDP.

A reasonable first pass is that a one percentage point of GDP increase in the fiscal deficit raises the current account deficit by half a percentage point. That is—more or less—what is in the IMF’s global current account model these days.*

But, as Dr. Krugman likes to note, there is no immaculate adjustment.

The rise in the trade and current account deficit doesn’t happen by magic—at least not beyond the direct impact of any demand stimulus that spills over to imports. Part of the impact on the external balance comes because a pro-cyclical fiscal expansion typically leads the central bank to raise interest rates to keep the economy from overheating, and thus a fiscal expansion pushes the currency up. But I wouldn’t be surprised if the IMF’s standard coefficient for all fiscal changes overestimates the trade impact of a big tax cut for corporations, pass-throughs, individuals who restructure themselves into pass-throughs, and those making more than $100,000. Fiscal stimulus only happens if the tax cut is spent not saved—and, well, a large share of the tax cut is likely to go to share buybacks and the like, not to financing new greenfield investment.

And there is another source of uncertainty: exchange rates move in response to what happens abroad, not just in the U.S.

If Europe continues a strong demand-led recovery and the ECB looks set to end its bond buying in 2018 and raise rates in 2019, the dollar might not go up by all that much even with the Trump tax plan. Conversely, if China over-tightens (always a risk) and its economy loses momentum and depreciation pressure resumes, the dollar move could be bigger than expected. Same for Japan if the planned 2019 consumption tax goes through and weakens Japan’s economy by more than expected.

But there is a second channel linking tax reform to the trade balance as well—one that matters less macroeconomically, but it is of interest to me.

Tax reform will also change the incentives firms face to shift profits around, and that in turn could impact the measured trade and current account balance.**

On the international side there will be real reform: the Senate Finance Committee and the House both proposed that the U.S. shift from a system of global tax with deferral of offshore profits (the deferral of offshore profits in effect meant that there hasn’t been global tax, and highly profitable firms deferred repatriation while waiting for a tax holiday) to a territorial system with a minimum tax on intangible income in low tax jurisdictions. The Senate Finance Committee also included a special low tax rate on earnings from the export of intangibles (intellectual property and the like) held by a firm in the United States.

I am also going to assume that the alternative corporate minimum tax (maintained at 20 percent in the bill that passed the Senate) doesn’t undo the other international tax reforms. That’s a big assumption, but, well, an alternative minimum tax that hits all global income repatriated back to the U.S. would be a radically different reform.

——

There are three broad categories of tax strategies that developed to in response to the old system of tax that in my view have had a large impact on the U.S. trade balance: transfer pricing and borrowing from foreign parents that limits the reported profits of foreign subsidiaries in the United States; transfer pricing that shifts profits on the export of intellectual property (notably on intellectual property related to smart phones and computer software) out of the United States to close-to-zero tax jurisdictions; and the offshoring of the production of high-value components to low-tax jurisdictions (notably shifting the production of things like the active ingredients in pharmaceuticals and the concentrate of soft drinks to tax havens).

I want to take a stab at how the changes in the Senate’s bill (key international sections are on p. 393 and p. 405) would impact each of these tax strategies. To be clear, I am not at all sure I have this right. I am not a tax lawyer and don’t pretend to understand how all the provisions in the Senate’s bill will interact.

Let’s take each of the main tax strategies in turn.

Shifting profits out of the U.S. subsidiaries of foreign multinationals (presumably to a jurisdiction with lower tax)

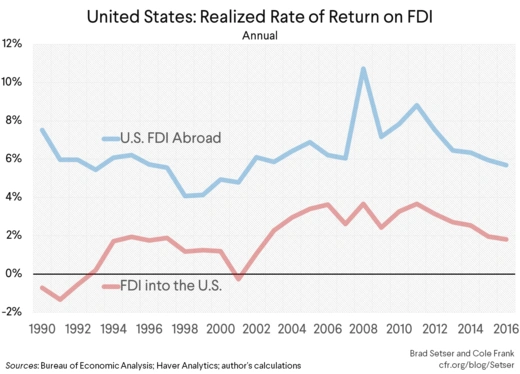

We know this happens now because the income that foreign firms report on their investments in the U.S. report is quite low. Judging from the balance of payments, most foreign firms really shouldn’t be investing in the U.S: they aren’t earning any more than they could make on a simple portfolio of long-term Treasuries, so why bother?

In reality of course, foreign firms likely do make substantial profits in the United States. They just don’t want to report those profits in the U.S. and pay U.S. tax.

There are a couple of ways foreign firms keep the profits in their U.S. subsidiaries down: most notably by overcharging their U.S. subsidiaries for imported components and by loading up their U.S. subsidiaries with (tax-deductible) debt.

A pharmaceutical company based in Ireland (for example) would charge its U.S. subsidiary a high price for importing active ingredients for a medicine even if the pills themselves are physically produced and packaged in the U.S. (Hey, that’s why the Ireland and Switzerland are the two biggest sources of imports to Puerto Rico).

Similarly, the intercompany loans that the U.S. subsidiaries of foreign firms have taken out from their parents are larger than the intercompany loans that U.S. firms have made to their foreign subsidiaries, and thus the interest bill on intercompany loans results in a net flow of payments out of the U.S.

Itai Grinberg recently testified:

“U.S. MNCs [multinational corporations] are much more constrained than foreign MNCs from stripping income out of the U.S. tax base. A foreign MNC can reduce the amount it owes to the U.S. government through deductible interest and royalty payments from its U.S. affiliates to its foreign affiliates, as well as by charging its U.S. affiliates prices for goods or services that include the value of foreign-owned intangibles in high-priced products for resale in the United States.”

On first glance the Republicans’ proposed reform is reasonably tough on such tax structures—the anti-base erosion provisions include penalties on large payments by U.S. subsidiaries of foreign firms back to their offshore parent. I cannot really evaluate whether these base erosion provisions will prove effective or will themselves be gamed. But I would not be surprised if the combination of a U.S. rate of 20 percent and these penalties on transferring profits out of the U.S. leads to somewhat higher reported profits on foreign direct investment in the U.S. and somewhat lower reported imports.

But there will be an easy way to track this—watch the reported profits of the U.S. subsidiaries of foreign firms operating in the U.S. If their income jumps in the next few years, it may well be tax-related.

Remember that the balance-of-payments effect of a lot of tax strategies has been to improve the income balance (by raising the reported profitability of U.S. firms abroad relative to the profitability of foreign firms in the U.S.) while increasing the trade deficit (by encouraging the importation of high value components from low tax jurisdictions and reducing reported exports of intangibles and high value components). Reversing these strategies consequently will change the measured trade balance but not the current account balance: the income surplus from FDI earnings abroad relative to foreign earnings in the U.S. will fall as the trade balance improves.

Shifting profits on intellectual property rights to the foreign subsidiaries of U.S. firms

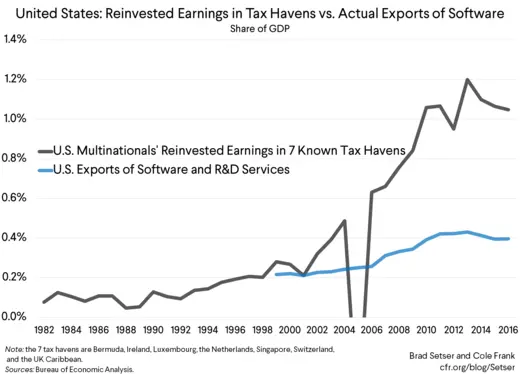

This is probably the biggest single tax-related distortion in the balance of payments. It likely reduces reported U.S. exports of intangibles (intellectual property and the like) by about a percentage point of GDP, while raising the foreign income of U.S. firms by an equal amount (e.g. tax shifting replaces taxable U.S. profits on exports with tax-deferred profits “earned” offshore).

Here is how the tax arbitrage often works: a U.S. firm with globally valuable intellectual property rights sells the foreign rights to its intellectual property at a low price to its subsidiary in a tax haven (that subsidiary itself is usually a holding company, hence the structure of global FDI flows) and the subsidiary in the tax haven (or subsidiaries in multiple tax havens) in turn get the profit from the firm’s global sales. The easiest structure to understand is a cost sharing agreement: Apple Ireland and Google Bermuda (and no doubt others) have received the global rights to the profits on their respective firm’s intellectual property in return for paying for a share of each firm’s research and development budget.*** If my math is right, for Apple Ireland this works out to a payment of about $5 billion back to Apple in California and an offshore profit stream of $35 to $40 billion. The net result is obvious in the balance of payments. The reinvested and, for now, tax-deferred profits U.S. firms report in low tax jurisdictions have soared relative to exports of either software or “research and development services.

The impact of the proposed reform here is complicated, as the reform has multiple components. Some should encourage firms to book profits in the U.S. rather than offshore, while others will encourage firms to continue to shift profits to low tax jurisdictions:

- Lowering the headline rate should make it more attractive to book profits in the U.S. rather than a subsidiary in a tax haven. But this effect is likely to be small. Twenty is well below 35. But most of the profit is likely with firms that have achieved effective tax rates on their offshore income of between 0 and 5 percent, which is much better than 20.

- The shift toward territoriality encourages firms to book profits abroad. Any profit earned abroad can now be repatriated to the U.S. without incurring additional tax (assuming the AMT is fixed!) and is free for distribution back to shareholders (or to fund investment in the U.S., though this second effect is likely to be small—the key firms here aren’t cash constrained). One thing is sure: If there is no incremental tax on repatriation, a lot of funds that are notionally now reinvested abroad (in tax havens) will be repatriated and corporate cash balances offshore will fall, with some impact on the global money market.

- The global minimum tax on intangible income (GITLI) should discourage tax shifting. Firms with no real assets abroad and big profits abroad in their offshore subsidiaries will have to pay 10 percent on their excess intangible profits (this makes the new tax system less than fully territorial). But this also could have the perverse effect of encouraging firms to shift tangible assets to low tax jurisdictions abroad (even more pharmaceutical production in low tax jurisdictions?) to raise the firms’ tangible income in the low tax jurisdictions. Remember tangible income offshore isn’t subject to the global minimum tax.

- Plus, as Gene Sperling has emphasized, to the extent that any reform allows firms to offset high taxes in one location abroad with low taxes in another location abroad, a firm with large untaxed profits in say Bermuda could lower its global tax burden by shifting profits out of the U.S. and toward say France. This would allow it to lower its overall tax burden toward the global minimum rather than to the U.S. headline rate (assessing the tax on a country by country basis solves this).

- The Senate also has proposed a low tax rate on intangible exports which should encourage, at the margin, firms to book their profits at home. The effective tax rate on profits earned on intellectual property retained by the U.S. firm in the United States falls to 12.5 percent (the Irish rate!) in the Senate’s proposal. That would encourage more profits to be booked in the U.S. if firms were actually paying the Irish rate abroad. But most firms pay far less. Bermuda’s corporate tax rate is zero. Apple has indicated that after it changed its tax structure it has paid Ireland about $1.5 billion over three years, or roughly 0.5 billion a year. A substantial sum no doubt, but not all that much relative to Apple’s likely “Irish” profit—and certainly not an effective tax rate of 12.5 percent.***

I do worry—though I confess that I don’t understand the calculation for “foreign-derived intangible income” and “deduction eligible income” and “qualified business asset income” well enough to have any confidence in this (help most appreciated!)—that the new low tax on intangible exports could create an incentive to book profits as intangible exports rather than as tangible exports. Better to export designs with a 12.5 percent tax rate than to export goods at say 20 percent? Though perhaps a portion of goods exports will be effectively taxed at the intangible rate as a portion of their value comes from the intellectual property embedded in the good?

It would help if I had a better concept in my mind of what will count as “deemed intangible income.”

So what’s likely to be the net effect?

I would expect some increase in U.S. exports of intangibles—whether from reduced exports of goods and more exports of intangibles as firms shift production abroad or from firms reshoring their IP and booking more of their current global profit in the U.S. (at the special 12.5 percent rate).

I would also certainly expect a shift from earnings reinvested abroad to earnings abroad that are paid as dividends back to the U.S. parent. That will end the most obvious “tell” of tax arbitrage in the balance of payments, namely the high absolute amount of reinvested earnings in low tax jurisdictions (where they clearly aren’t being reinvested in real assets). Ireland’s holdings of U.S. Treasuries are gonna fall…

But my best guess is that there will be only a modest change in total offshore earnings of U.S. multinationals. The current reform—in my view, so long as the alternative minimum tax is clarified—treats the foreign earnings of U.S. firms abroad fairly favorably, so I don’t think it will lead to an unwind of the tax strategies that have led to the development of large offshore profits.

There will be an easy way to tell: see how the total earnings of U.S. firms abroad evolves. If exports of services (notably software) rise and offshore earnings fall, the 12.5 percent rate on intangible income generated in the U.S. may have a bigger effect than I now anticipate.

And it also will be worth watching to see if the earnings U.S. firms report in relatively high tax jurisdictions rise as firms take advantage of the ability to offset profits in high tax jurisdictions abroad against profits in zero tax jurisdictions abroad. (The reported earnings of U.S. firms in places like Germany, France, Italy, Japan, and China are currently low relative to their reported earnings in low tax jurisdictions). See Stephen Rosenthal of the Tax Policy Center as well.

Offshoring of the production of high-value components to low-tax jurisdictions

Finally, there is the aspect of the current tax system that one might think President Trump would target: the tax system encouraged some firms to produce abroad in low tax jurisdictions for sale back to the United States.

We know this happens.

Pepsi’s global concentrate headquarters is in Ireland. And at least once upon a time, it was producing concentrate in Ireland for sale back to the U.S.—not just for sale to other European markets.****

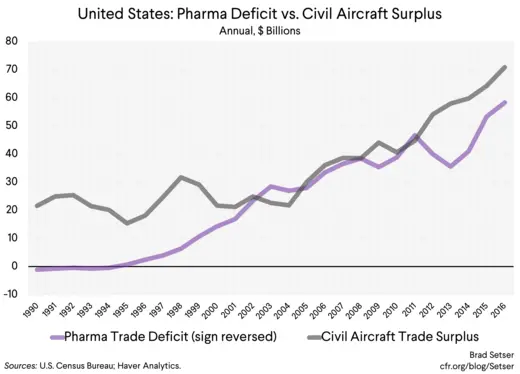

U.S. pharmaceutical firms that produce in low tax offshore jurisdictions clearly sell back to the U.S.—the U.S, after all, imports about $25 billion in pharmaceuticals from Ireland, and another $10 billion or so from Switzerland.

The fact that the U.S. trade deficit in pharmaceutical products is now only a bit smaller than the U.S. trade surplus in aircraft (counting the surplus in aircraft parts and engines) should be getting a lot more attention in my view.

And I suspect there are more subtle examples as well. Fabless semiconductor design firms outsource production rather than doing production in house—so the tax gain isn’t as obvious as it is with pharmaceuticals. And the semiconductors made by the firms’ offshore contractors are then sold to the Chinese electronics assembly line before the computer or smart phone that uses the chip comes back to the U.S. But the net effect is arguably similar to what happens with pharmaceutical: some fabless semiconductor firms reportalmost no taxable U.S. income even though they no doubt make a profit off the sale of electronics that use their chip designs in the U.S.

Such strategies do more than simply shift profits from one jurisdiction to another: offshore production of high-value components to meet U.S. demand raises the total trade and current account deficit (absent offsetting exchange rate changes) as there is a shift in the location of manufacturing value-added. The rise in goods imports back to the U.S. from such strategies should exceed the sum of the associated export of intangible income from the U.S. to the low tax jurisdiction (from the sale of the intellectual property rights) and the offshore profit earned by the offshore manufacturing subsidiary of the U.S. firms.

Does the proposed reform change the incentives that have led some firms to produce high value components for sale in the U.S. abroad? I think not. Remember that firms that produce goods abroad in a low tax jurisdiction won’t be taxed at all on the normal return of their tangible investment abroad, so producing abroad in a low jurisdiction is still better than producing in the U.S. at 20 percent. The “global” tax on excess intangible earnings is low relative to the U.S. rate. But it is possible that some of the base erosion provisions will bind here (help again would be appreciated).

In any case, I will be watching how the bilateral trade balance with low tax jurisdiction in pharmaceuticals evolves.

Now it is true that the sectors most prone to tax-shifting are fairly capital-intensive, and support relatively few jobs. But it is also true that these are the kind of sectors where twenty years ago globalization was thought to favor more not less U.S. production…

UPDATE: For more on the ability of firms to game the proposed international provisions by shifting production abroad, do read this paper by a group of tax law experts, including my co-author on tax and dark matter, David Kamin.

* Technically the fiscal coefficient in the IMF’s model is 0.47, so a bit under 0.5. The fiscal coefficient generally has been revised up in the IMF’s estimates over the past few years. If the IMF believed the right fiscal stance for the U.S. was fiscal balance—as required in the Eurozone—the U.S. fiscal gap would on its own account for most of the current account deficit. But the IMF thinks the “optimal” fiscal deficit for the U.S. is around 2 percent of GDP.

** Around 70 percent of U.S. exports of research and development services go to low tax jurisdictions, led—of course—by exports to Ireland.

*** Tis a topic for another time but I think the evidence is pretty strong that the Irish leprechaun is really an apple. Thanks to the Paradise Papers we know Apple did a tax reorganization that turned one of their foreign subsidiaries into a tax resident of Ireland a few years back, right around the time of the huge changes in Ireland’s GDP and balance of payments.

**** Ireland’s exports of “other food” to the U.S. (end-use category 00180, now well over $2 billion) are suspiciously high. Higher than France or Italy for example. Irish food is a bit underrated, but it is hard to think Ireland really does better here than these (much) bigger European countries with a global culinary reputation. I wouldn’t be surprised if “other food” includes a bit of concentrate.

Brad W. Setser is a senior fellow at the Council on Foreign Relations. His expertise includes macroeconomics, global capital flows, financial vulnerability analysis, sovereign debt restructuring, and the management of financial crises. He regularly blogs at Follow the Money.

© 2017 Council on Foreign Relations. All rights reserved

The paper was originally posted here.